At some point, a house that once felt perfect just… doesn’t anymore.

At some point, a house that once felt perfect just… doesn’t anymore.

You may have heard homeowners today have a lot of equity built up. But what does that really mean? Let’s break it down.

After a long stretch where buyers were competing for too few homes, inventory has made a comeback over the past year.

Buying your first home can feel frustrating when the numbers don’t line up the way you expected.

If you’re planning to buy a home this year, you may be focused on the spring market.

There’s finally a little good news for anyone who’s been priced out or sitting on the sidelines.

Buying a home is one of the biggest purchases you’ll ever make. And homeowner’s insurance is what protects that investment.

For a growing number of homeowners, retirement isn’t some distant idea anymore. It’s starting to feel very real.

According to Realtor.com and the Census, nearly 12,000 people will turn 65 every day for the next two years. And the latest data shows as many as 15% of those older Americans are planning to retire in 2026. And another 23% will do the same in 2027.

If you’re considering retiring soon too, here’s what you should be thinking about.

Now’s the perfect time to reflect on what you want your life to look like in retirement. Because even though your finances will be going through a big change, you don’t necessarily want to feel like you’re living with less.

But odds are, what you do want is for life to feel easier.

Easier to enjoy.

Easier to manage.

Easier to maintain day-to-day.

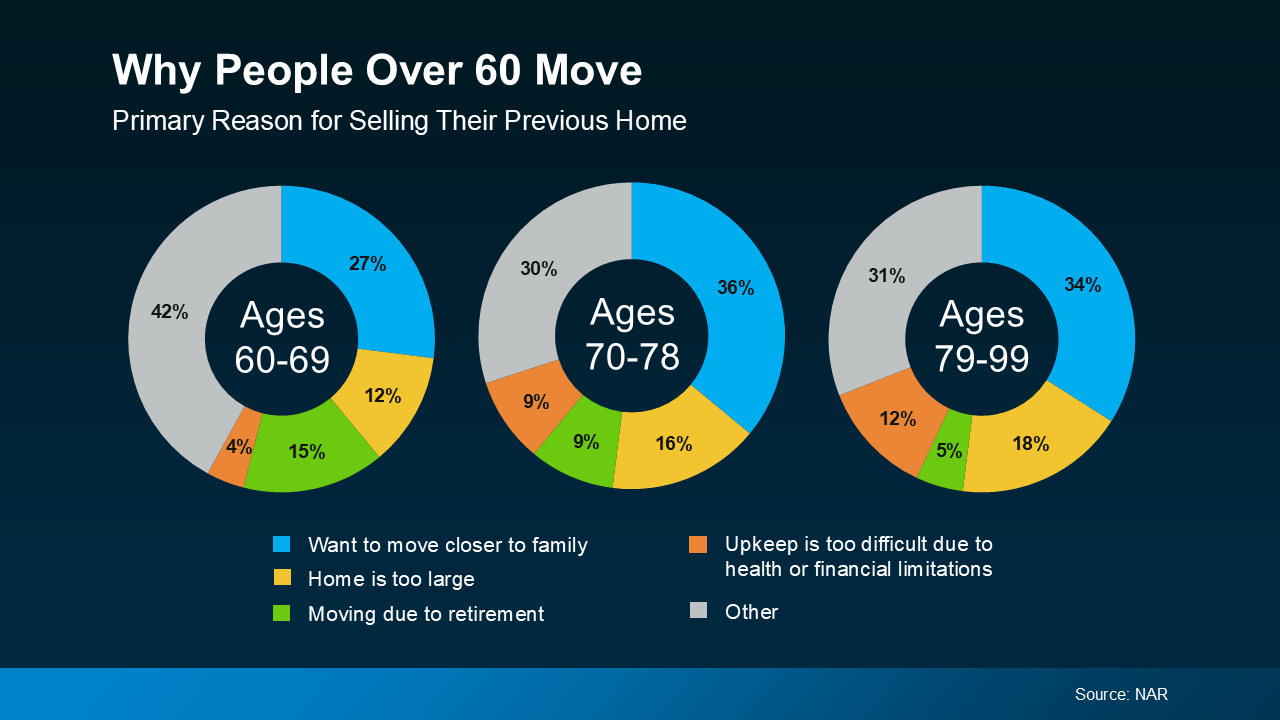

You can see these benefits show up in the data when you look at why people over 60 are moving. The National Association of Realtors (NAR) finds the top 4 reasons aren’t about timing the market or chasing top dollar. They’re about lifestyle:

No matter the reason, the theme is the same: downsizing isn’t about giving something up. It’s about gaining control and choosing simplicity. And it brings peace of mind to know your home fits the years ahead, not the years behind.

And the best part? It’s more financially feasible now than many homeowners would expect.

Here’s the part that makes it possible. Thanks to how much home values have grown over the years, many longtime homeowners are realizing they’re in a stronger position than they thought to make that move.

According to Cotality, the average homeowner today has about $299,000 in home equity. And for older Americans, that number is often even higher – simply because they’ve lived in their homes longer.

When you stay in one place for years (or even decades), two things happen at the same time:

That combination creates more options than you’d expect, even in today’s market.

So, whether you just retired, or you’re about to, it’s not too soon to start thinking about what comes next. Sure, it can be hard to leave the house you made so many years of memories in, but maybe it’s time to close one chapter to open a new one that’s just as exciting.

Downsizing is about setting yourself up for what comes next – on your terms.

If retirement is on the horizon and you’ve started wondering what your current house (and your equity) could make possible, the first step isn’t selling. It’s understanding your options.

It’s time to talk to an agent. A simple, no-pressure conversation can help you see what downsizing might look like – and whether it makes sense for you.

Who doesn’t love a top 10 list? Well, here are two top 10 lists for the housing market this year. But before you take a look, there’s something you should know.

If a move is on your radar for 2026, here’s the most important thing you need to understand upfront: there isn’t one housing market this year – there are many.

Experts agree 2026 is shaping up to be one of the most geographically split housing markets in years. Some areas are tilting in favor of sellers, while others are opening real doors for buyers. Who has the advantage depends almost entirely on where you are. Selma Hepp, Chief Economist at Cotality, puts it this way:

“Looking ahead to 2026, regional differences will remain pronounced, with demand favoring areas that offer both economic opportunity and relative affordability.”

To show just how divided the landscape is, here’s a look at where sellers are expected to have the upper hand, and where first-time buyers may finally find their opening this year.

Zillow identified the following metros as some of the strongest seller markets for 2026, based on buyer demand, pricing momentum, and how quickly homes are expected to sell:

In markets like these, buyers are going to be competing for limited inventory, which gives sellers more leverage.

In markets like these, buyers are going to be competing for limited inventory, which gives sellers more leverage.

Homeowners in seller’s markets this year can expect:

Stronger buyer interest

Shorter time on market

Better odds of selling close to (or above) asking price

That doesn’t mean every listing is guaranteed success. But it does mean sellers who prepare well and lean on an agent’s expertise should be very happy with their results in 2026.

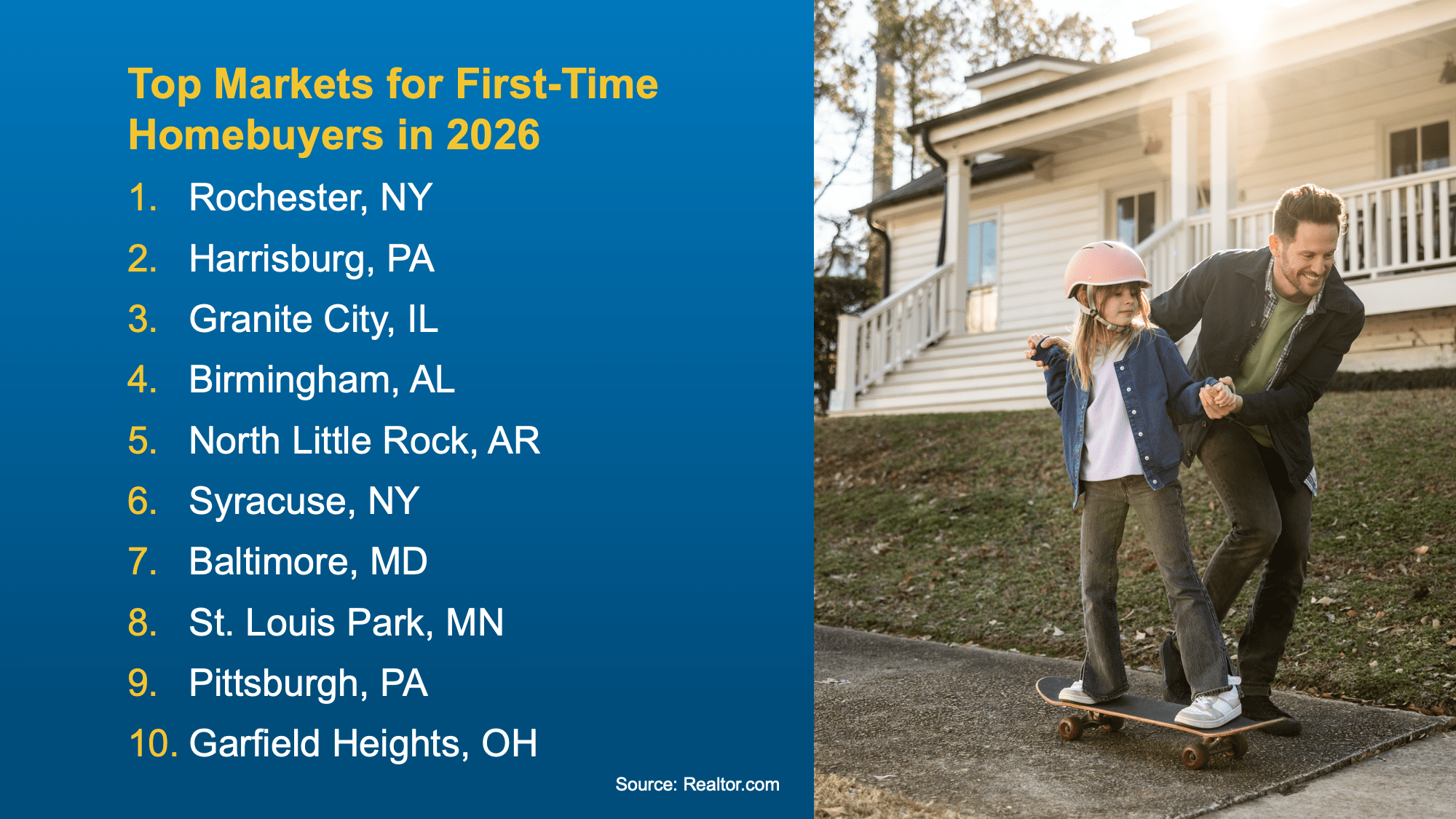

On the flip side, here’s a look at where buyers have the power – in particular, first-time buyers, since they’ve had the hardest time breaking into the market lately. Realtor.com highlights the top metros where first-time buyers are expected to have better opportunities in 2026:

These markets stand out for a mix of:

These markets stand out for a mix of:

More affordable home prices

Better housing availability

Strong local amenities and economic health

For first-time buyers, that combination matters. It’s what could finally turn “someday” into “this could actually work.” In buyer’s markets, they should expect:

Less intense competition

More room to negotiate

A clearer path to getting an offer accepted

What Matters More Than Any Top 10 List

Not seeing your city on the list? Don’t stress. This is just a national snapshot, not a judgment on your local market. The goal here is just to show you how different the market really is depending on where you are.

And remember, you can buy or sell no matter how your local market leans. You just need an agent’s help to figure out the right strategy to get it done. For example:

A seller in a more buyer-friendly metro may need to be aggressive on their price and prep.

A buyer in a seller-leaning area may still need to come prepared with their best offer.

To find out where your market falls and what you should expect, you’ll want the help of a local expert.

The housing market in 2026 isn’t one-size-fits-all. It’s a year where local conditions matter more than ever.

Whether your market leans more buyer-friendly or seller-friendly, the right strategy can put you in a strong position. And that’s where a local expert comes in. Connect with a trusted real estate agent today.

When you see a house that’s been sitting on the market for a while, the reaction is almost automatic. You start thinking:

What’s wrong with it?

Why hasn’t anyone bought it yet?

Am I missing something?

That mindset made sense a few years ago. But in today’s market, you may actually miss out.

More Time on Market Isn’t Automatically a Concern Anymore

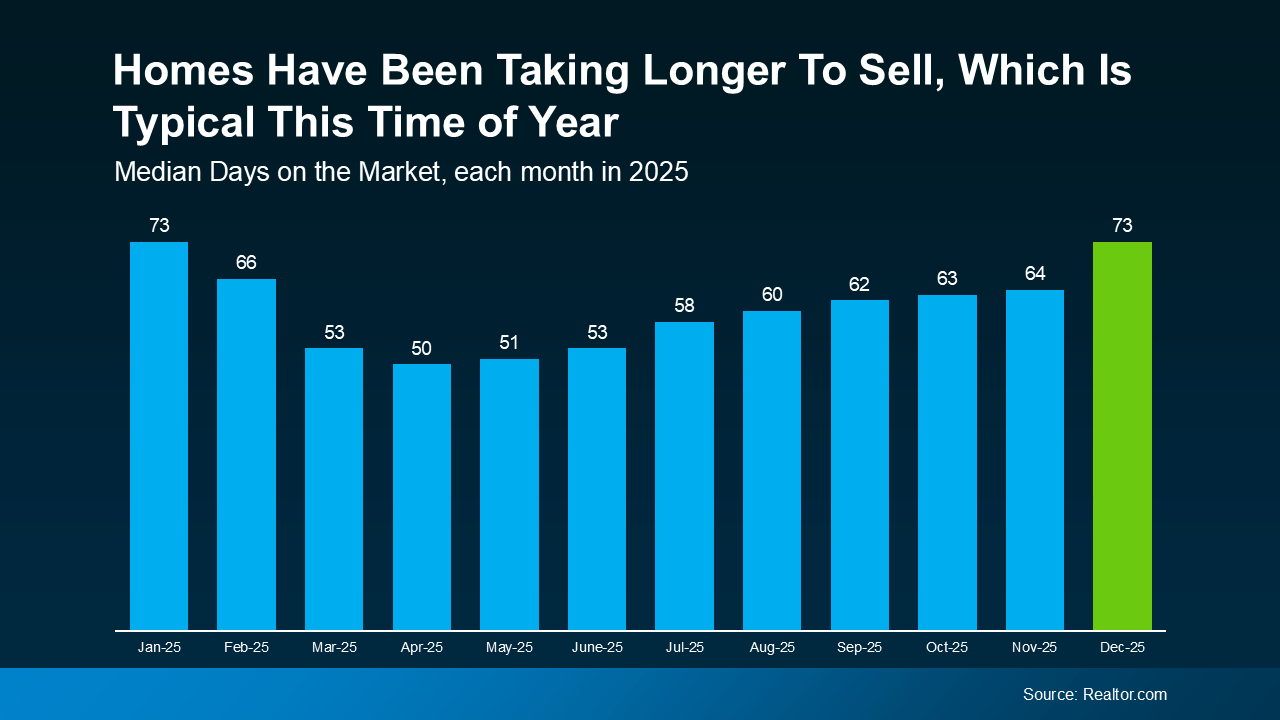

A few years ago, homes sold in just a matter of days. Sometimes, hours. Anything that lingered longer than that raised concerns. But that’s no longer the baseline.

Inventory has grown. Buyers have more choices. And homes are taking longer to sell across the board. Those are some of the reasons why the typical time it takes a home to sell has climbed this year:

And it’s not that 73 days is slow. That’s actually pretty normal for this time of year. It just feels slow because you heard so much about houses being snapped up in the buying frenzy a few years ago.

And it’s not that 73 days is slow. That’s actually pretty normal for this time of year. It just feels slow because you heard so much about houses being snapped up in the buying frenzy a few years ago.

That shift alone explains a lot of what you’re seeing. It’s not necessarily that there’s anything wrong with the house itself. Although, let’s be honest, sometimes that is the case.

Most of the time today, a house that’s taking longer to sell simply means:

There are a lot of homes for sale in that area

The seller priced a little too high at first

The home didn’t photograph as well online

Buyers passed it over for flashier listings nearby

The timing just wasn’t right when it first hit the market

None of those are necessarily deal-breakers.

What Buyers Often Get Wrong About These Listings

Because even though you may assume a house that hasn’t sold must have hidden issues, the reality is, that’s not always the case. And, if the house does have issues, it’ll show up quickly in your inspection.

That’s information you can use to negotiate. Not a reason to walk away automatically. And in many cases, that’s where buyers find the best deals.

The key is knowing which homes that have been sitting for a while are worth a second look – and which ones aren’t. That’s why working with a local agent makes a real difference. They’ll be able to look at disclosures and more to help you uncover hidden gems other buyers may overlook.

A home sitting on the market isn’t always a warning sign. Sometimes it’s an overlooked opportunity.

If you want help identifying which homes are worth a second look (and which ones to skip), talk to a local agent.